ALS Limited announces solid FY24 results amid market challenges, introduces new growth framework

ALS Limited today announced its financial result for the 12 months to 31 March 2024.

ALS Chairman, Bruce Phillips, said: “This was a solid performance by our global business despite the continued challenging market environment.

Underlying NPAT was down only 1.3%, reflecting the strength and diversity of our portfolio. The operating performance, solid financial position and encouraging outlook supports the declaration of a 19.6 cps final dividend for our shareholders. This has been achieved whilst continuing to increase our growth investments.”

CEO and Managing Director, Malcolm Deane said: “The Group has continued to deliver revenue growth and maintain industry-leading margins despite challenging market conditions.

“Our balance sheet remains well positioned, benefiting from high cash flow generation.

“While near term focus is on integrating recent acquisitions, the balance sheet and cash flow strength supports future growth from disciplined allocation of capital in accordance with our new value creation framework.

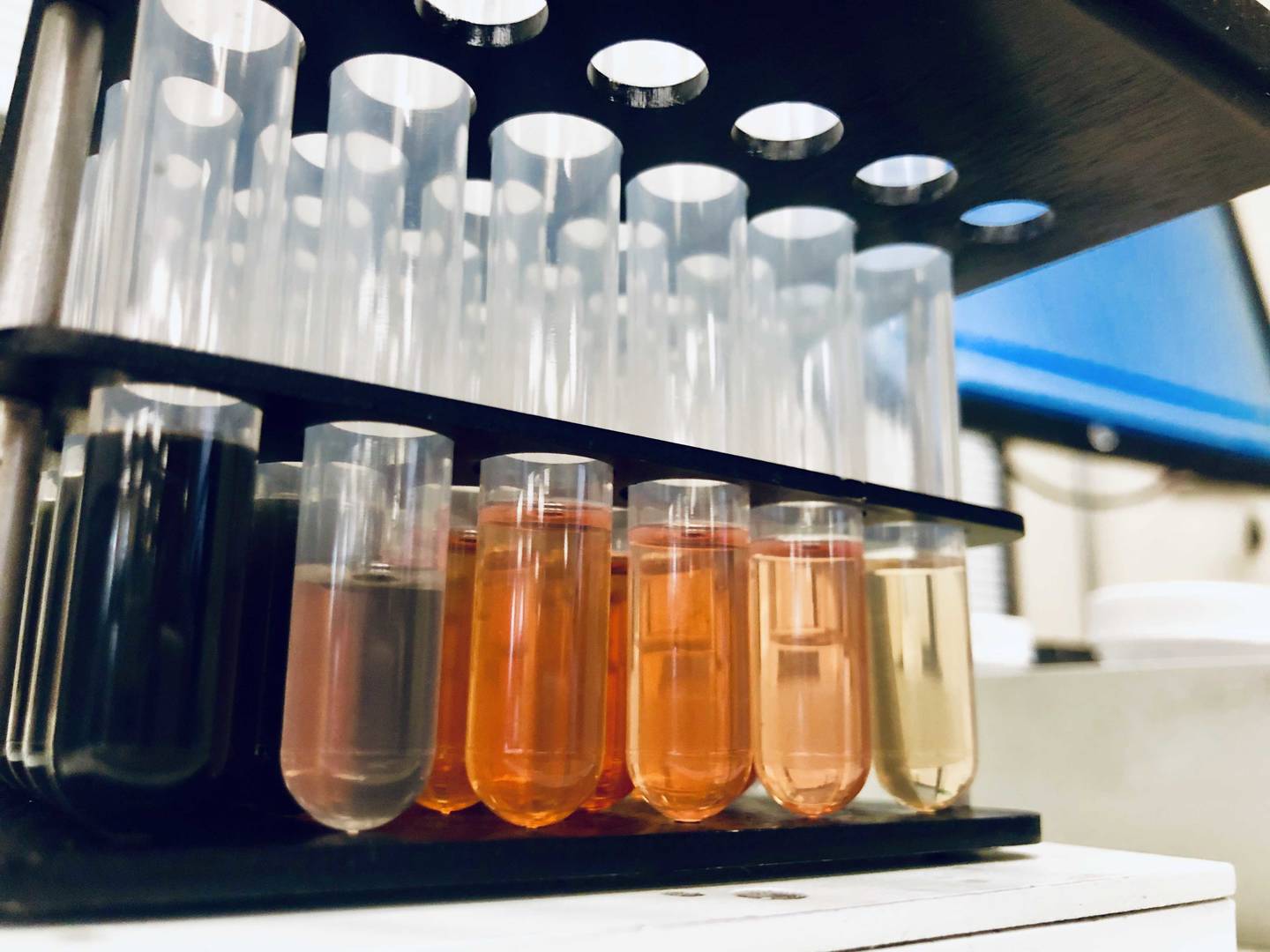

“Our Commodities division has again proven to be a global market leader in Minerals testing. Whilst soft capital markets continued to limit exploration activities the business was able to grow market-share, with sustained client demand for additional high-value services largely offsetting weaker sample volumes.

“Further demand for our industry-leading services, including high-performance method testing, has supported our strong market share growth. Additionally, we continued to deploy growth capital to support development of new mine-site production testing facilities.

“Collectively, the financial results demonstrate resilience and reduced cyclicality within the Minerals portfolio.

“Within Life Sciences, our Environmental business has continued its strong growth momentum with further margin improvement through leveraging its global scale and client value proposition.

“Pleasingly, Food was able to maintain its recovery throughout the second half of the year, achieving good growth and margin improvement supported by the regionally strong European businesses.

“The Pharmaceutical business remains impacted by challenging market conditions associated with new product development and operational inefficiency. To address this, the integration and transformation of Nuvisan is now underway.

“The Group has made excellent progress towards its FY27 vision, including the financial objectives. Whilst we have made some refinements to the strategy, including the addition of a new value creation framework, our commitment to the FY27 vision remains.”

1 Attributed to equity holders of the Company and excluding restructuring and other one-off items (SaaS/ERP implementation), divestment and impairment losses and amortisation of acquired intangibles

The existing FY27 strategy has served the Group well, with all financial metrics well on track. Following a period of reflection and refinement, the Group has refreshed its framework to tweak some elements of the strategy going forward. The new framework is supported by:

The framework combines a risk-weighted approach to capital allocation that will protect, extend and expand the portfolio. Overall, the Group expects to deliver mid-to-high single digit organic revenue growth, achieve a steady improvement in operating margins, and strong ongoing cash generation. Allocation of growth capital will be deployed seeking a minimum return on capital employed of 15%, ensuring maximum growth and returns for shareholders over the medium term.

The existing financial targets set for FY27 remain unchanged. These included: growing revenue to $3.3 billion, and growing underlying EBIT to $0.6 billion, with a group margin floor of 19%. In addition, the Group will aim to keep cash conversion above 90% and continue to improve the return on capital above 20%.

FY24 highlights1

- Underlying Revenue2 of $2,586 million, an increase of 6.8% supported by most businesses, acquisitions, and FX tailwinds.

- Statutory net profit after tax (NPAT) of $12.9 million, a decrease of $278.3 million, impacted predominantly by the impairment of the initial 49% of Nuvisan and restructuring provisions ($248.8 million), and other increased one-off items.

- Underlying EBIT3 of $491.8 million, a slight increase of 0.2%. The operating margin was 19.0%, in line with the Group floor target, representing a decline of 125 bps compared to prior year. Margin contraction was partially offset by strong performances within Environmental, Food and Industrial Materials, whilst Minerals provided a resilient result.

- Underlying NPAT of $316.5 million, a slight decrease of 1.3%, impacted by mixed market conditions.

- Executed eight acquisitions, expecting to contribute an additional ~$152 million revenue on a full year run-rate basis.

- Strong balance sheet, supporting growth agenda in-line with value creation framework, with 2.0x leverage ratio and available liquidity of over $530 million.

- Final dividend of 19.6 cps (partially franked to 20%), representing a payment of $94.9 million to shareholders.

- Maintained carbon neutrality for scope 1 and 2 emissions.

- Industry leading health and safety outcomes, with a 5% reduction on TRIFR4.

ALS Chairman, Bruce Phillips, said: “This was a solid performance by our global business despite the continued challenging market environment.

Underlying NPAT was down only 1.3%, reflecting the strength and diversity of our portfolio. The operating performance, solid financial position and encouraging outlook supports the declaration of a 19.6 cps final dividend for our shareholders. This has been achieved whilst continuing to increase our growth investments.”

CEO and Managing Director, Malcolm Deane said: “The Group has continued to deliver revenue growth and maintain industry-leading margins despite challenging market conditions.

“Our balance sheet remains well positioned, benefiting from high cash flow generation.

“While near term focus is on integrating recent acquisitions, the balance sheet and cash flow strength supports future growth from disciplined allocation of capital in accordance with our new value creation framework.

“Our Commodities division has again proven to be a global market leader in Minerals testing. Whilst soft capital markets continued to limit exploration activities the business was able to grow market-share, with sustained client demand for additional high-value services largely offsetting weaker sample volumes.

“Further demand for our industry-leading services, including high-performance method testing, has supported our strong market share growth. Additionally, we continued to deploy growth capital to support development of new mine-site production testing facilities.

“Collectively, the financial results demonstrate resilience and reduced cyclicality within the Minerals portfolio.

“Within Life Sciences, our Environmental business has continued its strong growth momentum with further margin improvement through leveraging its global scale and client value proposition.

“Pleasingly, Food was able to maintain its recovery throughout the second half of the year, achieving good growth and margin improvement supported by the regionally strong European businesses.

“The Pharmaceutical business remains impacted by challenging market conditions associated with new product development and operational inefficiency. To address this, the integration and transformation of Nuvisan is now underway.

“The Group has made excellent progress towards its FY27 vision, including the financial objectives. Whilst we have made some refinements to the strategy, including the addition of a new value creation framework, our commitment to the FY27 vision remains.”

Overview of FY24 results

| A$ million | FY24 | FY23 | Change | CCY change |

| Revenue | 2,586.0 | 2,421.2 | 6.8% | 4.4% |

| Underlying EBIT | 491.8 | 490.7 | 0.2% | 0.2% |

| Margin | 19.0% | 20.3% | (125) bps | (81) bps |

| Statutory NPAT | 12.9 | 291.2 | (95.6)% | |

| Underlying NPAT | 316.5 | 320.6 | (1.3)% | |

| Basic EPS (cents per share)5 | 65.4 | 66.3 | (1.4)% | |

| Free cash flow | 532.4 | 550.5 | (3.3)% | |

| Underlying ROCE | 20.6% | 20.5% | 10 bps | |

| DPS | 39.2 | 39.7 | (1.3)% | |

| Net Debt | 1,175 | 1,023 | 14.89% |

FY27 vision and updated framework

Over the last two years, the Group has continued to make significant strides in delivering the FY27 vision. Through this journey, ALS’ innovative and data driven approach has provided meaningful growth opportunities such as industry-leading testing capabilities, advancement of the global Laboratory Information Management Systems, and development of AI and machine learning capabilities. The Group has also reshaped the portfolio and deployed significant capital towards both organic and inorganic growth.The existing FY27 strategy has served the Group well, with all financial metrics well on track. Following a period of reflection and refinement, the Group has refreshed its framework to tweak some elements of the strategy going forward. The new framework is supported by:

- A newly formed executive team that joins together both long-term and new leaders.

- Scaling businesses in Minerals and Environmental, and regionally strong businesses in Life Sciences, to deliver solid organic growth.

- Ongoing focus to improve integration of acquisitions.

- Enhancements to our operating model that will extract margin improvement on some underperforming businesses and further margin uplift on already industry-leading margins.

- A consistent approach to marketing to clients, which includes dynamic pricing.

- An updated approach to capital allocation, referred to as the ‘value creation framework’.

Value creation framework

The value creation framework provides the fundamentals to help enable delivery of the ambition of achieving top quartile shareholder returns over the medium term.The framework combines a risk-weighted approach to capital allocation that will protect, extend and expand the portfolio. Overall, the Group expects to deliver mid-to-high single digit organic revenue growth, achieve a steady improvement in operating margins, and strong ongoing cash generation. Allocation of growth capital will be deployed seeking a minimum return on capital employed of 15%, ensuring maximum growth and returns for shareholders over the medium term.

The existing financial targets set for FY27 remain unchanged. These included: growing revenue to $3.3 billion, and growing underlying EBIT to $0.6 billion, with a group margin floor of 19%. In addition, the Group will aim to keep cash conversion above 90% and continue to improve the return on capital above 20%.

Divisional review

Commodities:| A$ million | FY24 | FY23 | Change | CCY change |

| Revenue | 1,086.6 | 1,087.1 | (0.0)% | +0.7% |

| Underlying EBITDA | 383.9 | 390.3 | (1.6)% | +0.4% |

| Margin | 35.3% | 35.9% |

(57) bps | (12) bps |

| Underlying EBIT | 318.7 | 330.0 | (3.4)% | (0.8)% |

| Margin | 29.3% | 30.4% | (103) bps | (45) bps |

Revenue was flat vs pcp but delivered modest organic revenue growth of 0.3%, scope growth of 0.4% offset by an unfavourable currency impact of 0.7%. Growth was limited due to the extended slowdown in mining exploration activities due to soft capital markets. The expected sample volume decline was largely offset by increased market-share, dynamic price management and further uptake of complementary value-added services by clients.

Underlying EBIT decreased by 3.4% to $319 million, with the overall margin contracting to 29.3%, with FX headwinds attributable for 57 bps. Margins continue to be resilient which reflects the reduced cyclicality to exploration activities through downstream growth, flexibility of the cost base and increased uptake of new service offerings, e.g. high-performance method testing.

Minerals organic revenue declined by 2.4%, impacted by the continued slowdown of exploration activities, with sample volumes declining by 8.4%. The business minimised the expected slowdown in the period through increasing market-share, pricing discipline, cost management, effective capacity planning and downstream activity growth. Margins benefited from price / client mix following increased uptake of premium value-added services and additional mine-site production expansion. The Metallurgy business performed well, growing both revenues and EBIT, noting a slowdown in 2H24.

Industrial Materials delivered organic revenue growth of 13.4%, with growth and margin improvement achieved across most businesses. Inspections benefited from strong global commodity trading activities, Oil & Lubricants performed well and achieved market share growth (in APAC, North America and Latin America), and Coal was supported by buoyant prices and volume recovery.

Life Sciences:

| A$ million | FY24 | FY23 | Change | CCY change |

| Revenue | 1,499.4 | 1,334.1 | +12.4% | +7.4% |

| Underlying EBITDA | 330.7 | 302.9 | +9.2% | +4.2% |

| Margin | 22.1% | 22.7% | (65) bps | (68) bps |

| Underlying EBIT | 226.2 | 206.9 | +9.3% | +4.4% |

| Margin | 15.1% | 15.5% | (42) bps |

(43) bps |

Revenue growth of 12.4% with organic revenue growth of 3.6%, scope growth of 3.7% and a favourable currency impact of 5.0%. Growth was driven by strong performances from both the Environmental and Food businesses, but partially offset by the continued slowdown in new product development revenues in the Pharmaceutical business.

Underlying EBIT increased by 9.3% to $226 million, with the overall margin contracting to 15.1% due to challenging market conditions impacting the Pharmaceutical business. Margin improvement was achieved within the rest of the Life Sciences division.

Environmental business delivered strong organic revenue growth of 8.6%, with growth achieved across all regions. Growth outpaced the overall market, and was supplemented with acquisitions in key growth geographies. The business was able to further expand margins during the period through leveraging its global scale and further process standardisation.

Food business delivered strong organic revenue growth of 6.5%, with volume and price growth recovery accelerating in the European markets.

Pharmaceutical business had an organic revenue decline of 11.5%, a result of challenging market conditions within the sector.

Nuvisan. During the period the Group acquired the remaining 51% interest in Nuvisan at nil cost. Taking full control and ownership of Nuvisan provided the best opportunity to deliver earnings growth and maximise shareholder value optionality. With full ownership of Nuvisan, the Group has commenced implementation of a transformation program to increase revenue from targeted investment in business development and improve profitability across the business. The program is expected to deliver annual cost savings of ~€25 million with a total restructuring cost of ~€20 million over a two-year period. The program is expected to conclude in 2026.

Capital allocation, growth and balance sheet

The Group continued to demonstrate its disciplined and proactive approach to capital allocation, in-line with the updated value creation framework (highlighted above). Through this framework, the Group has successfully deployed growth capital, both organic and through value-added acquisitions, returned capital to shareholders with dividends at the top of the payout range, and with leverage operating at the mid-point of the target range (1.7 to 2.3x)6.The Group’s total capital expenditure increased in FY24 to $152 million compared to $146 million in pcp. Most of the growth capital was allocated to the Environmental and Minerals businesses, in-line with the updated value creation framework. Capital also supported initiatives to improve underlying operations and align businesses with the ‘ALS Way’. The Group completed eight acquisitions7, that are expected to contribute $152 million in revenue on a full year basis (including the remaining 51% interest of Nuvisan) at a total cost of approximately $76 million. The acquisitions predominately focused on geographic expansion and new service offerings within the Environmental business.

As announced on 1 April 2024, the Life Sciences businesses of York (northeast USA) and Wessling (Germany, France and Switzerland) were acquired. The York acquisition completed on 1 April while Wessling, which requires regulatory approvals, is on track for completion in June 2024. These acquisitions are expected to contribute $195 million in revenues on a full-year basis. While these acquisitions are expected to meet targeted returns in the medium-term, initially, on a combined basis, they will have an adverse impact on operating margins and be earnings dilutive (inclusive of the cost of debt funding).

As at 31 March 2024, the balance sheet remains strong with a leverage ratio of 2.0x, with over $530 million of available liquidity, including $346 million of undrawn bank facilities. Post completing the acquisitions of York and Wessling, leverage will be at the top of our stated range at 2.3x.

In April 2024, the Group entered into new additional bilateral revolving bank facilities totaling US$300 million (A$460.9million). These new facilities will be used to refinance current bank debt maturing in May 2024, and also fund the acquisitions of both York and Wessling. This refinancing completed in April 2024 will increase overall liquidity and remove any near-term refinance risk.

The Group is committed to reducing leverage to mid-point of target gearing range over the medium term.

Final dividend

Based on operations, solid financial position, and outlook, the Directors have declared a final dividend for the year of 19.6 cents per share, partially franked to 20% (2023 final dividend: 19.4 cents per share, 10% franked). Together with the interim dividend of 19.6 cents per share (20% franked), the partly franked dividend for the year will be 39.2 cents per share, down 1.3% on the pcp (2023: 39.7 cents), representing a combined dividend payout ratio of 60% of underlying NPAT, at the top end of the reference range (50 – 60% of underlying NPAT). The dividends will be paid on 2 July 2024 on all shares registered in the Company’s register at the close of business on 13 June 2024.

The Board has determined to re-activate the dividend reinvestment plan (DRP), providing maximum future capital flexibility for the business. Eligible shareholders will be able to elect to receive the final FY24 dividend under the DRP at a nil discount to the 5-business day VWAP, calculated post the DRP election date of 14 June 2024 (i.e. 17 - 21 June 2024 inclusive).

Investor Relations

ALS Limited

The Board has determined to re-activate the dividend reinvestment plan (DRP), providing maximum future capital flexibility for the business. Eligible shareholders will be able to elect to receive the final FY24 dividend under the DRP at a nil discount to the 5-business day VWAP, calculated post the DRP election date of 14 June 2024 (i.e. 17 - 21 June 2024 inclusive).

Perspectives for FY25

The medium to long-term outlook for both Life Sciences and Commodities remains positive. The Group’s portfolio remains well leveraged to attractive end markets, supported by industry tailwinds. The Group is well positioned to execute on near-term financial objectives:- Targeting mid-single digit organic revenue growth for the Group.

- Excluding acquisitions, modest improvement in operating margins for Life Sciences, with continued margin resilience in Minerals.

- Risk-weighted growth prioritisation to Environmental and Minerals businesses, in-line with the value creation framework.

- Strong focus on integration of acquisitions and Nuvisan transformation program.

- Leverage expected to operate at top end of targeted range.

For further information please contact:

Investor Relations

ALS Limited

About ALS Limited

A global leader in testing, ALS provides comprehensive testing solutions to clients in a wide range of industries around the world. Using state-of-the-art technologies and innovative methodologies, our dedicated international teams deliver highest-quality testing services and personalized solutions supported by local expertise. We help our clients leverage the power of data-driven insights for a safer and healthier world.

A global leader in testing, ALS provides comprehensive testing solutions to clients in a wide range of industries around the world. Using state-of-the-art technologies and innovative methodologies, our dedicated international teams deliver highest-quality testing services and personalized solutions supported by local expertise. We help our clients leverage the power of data-driven insights for a safer and healthier world.